Time Article the 25 People to Blame for the Financial Crisis

Time Article the 25 People to Blame for the Financial Crisis:

TIME's picks for the top 25 people to blame for the financial crisis includes everyone from former Federal Reserve chairman Alan Greenspan and former President George W. Bush to the former CEO of Merrill Lynch and you — the American consumer. As you read our choices, we'd like to know who you think deserves the most blame, and the least. After voting on the relative guilt (or innocence) of each person, view the full results here.

Jimmy Cayne We Must never forget what these men did to Main Street America These men took Bonus in the Millions while Americans were made homeless Bernie Madoff stole from "Rich Jews" who were paid back by the Government as they knew and Covered-up for him for over 10 years The Government has allowed these men, the banks, the servicers with the help of EACH STATES ATTORNEY GENERAL & LEGISLATURE TO BE PAID OFF - by the banks and the Federal Government The WSJ and others have exposed the Judge's Payoffs in stock and their conflicts:

1. The Wall Street Journal, published on November 2, 2021, “Hidden Interests - Federal Judge Files Recusal Notices in 138 Cases After WSJ Queries. Rodney Gilstrap initially argued he didn’t violate financial-conflicts law”; James.Grimaldi@wsj.com, Joe.Palazzolo@wsj.com, Coulter.Jones@wsj.com. (See the articles referred to in this section here and at Appendix:6§C.22.)

2. Thomson Reuters, with 2,500+ journalists and 600+ photojournalists, published on June 30, 2020, the first of its three-part report “The Teflon Robe”, John.Shiffman@thomsonreuters.com and Michael.Berens@thomsonreuters.com, on its massive investigation of state judges. It found that “hardwired judicial corruption” intertwines state judges and the state commissions on judicial performance that are duty-bound to supervise and discipline them. Reuters asked readers to send it their stories of abuse by judges…and it was “inundated” with them because those with stories want to tell them.

3. The Boston Globe published on September 30, 2018, its investigative report “Inside our secret courts”, Jenn Abelson, Nicole Dungca and “Todd Wallack” <twallack@gmail.com>, patricia.wen@globe.comrs.com, spotlight@globe.com, in whose “private criminal hearings, who you are –and who you know– may be just as important as right and wrong”.

4. Senator Elizabeth Warren, in her “I have a plan for the Federal Judiciary too”, dare denounce judges’ unaccountability and their abuse of it by refusing to recuse themselves from cases in which they own stock in one of the parties before them in order to steer the cases so as to protect and/or increase the value of their stock. Sen. Warren refers to their grabbing as ‘abusive self-enrichment.

5. The International Consortium of Investigative Journalists (ICIJ), in Washington, D.C., published on October 3, 2021, the Pandora Papers, that is, close to 12 million financial documents leaked to it. “More Than 600 Reporters Around The Globe Work With ICIJ On The Most Expansive Leak Of Tax Haven Files In History”. The expertise that ICIJ has gained in applying document scanning software and money tracking techniques can be applied to exposing judges’ illegal flow of money.

Meet the father of mortgage-backed bonds. In the late 1970s, the college dropout and Salomon trader coined the term securitization to name a tidy bit of financial alchemy in which home loans were packaged together by Wall Street firms and sold to institutional investors. In 1984 Ranieri boasted that his mortgage-trading desk "made more money than all the rest of Wall Street combined." The good times rolled: as homeownership exploded in the early '00s, the mortgage-bond business inflated Wall Street's bottom line. So the firms placed even bigger bets on these securities. But when subprime borrowers started missing payments, the mortgage market stalled and bond prices collapsed. Investment banks, overexposed to the toxic assets, closed their doors. Investors lost fortunes.

The programming czar at Scripps Networks, which owns HGTV and other lifestyle channels, helped inflate the real estate bubble by teaching viewers how to extract value from their homes. Programs like Designed to Sell, House Hunters and My House Is Worth What? developed loyal audiences, giving the housing game glamour and gusto. Jablin didn't act alone: shows like Flip That House (TLC) and Flip This House (A&E) also came on the scene. To Jablin's credit, HGTV, which airs in more than 97 million homes, also launched Income Property, a show that helps first-time homeowners reduce mortgage payments by finding ways to economically add rental units.

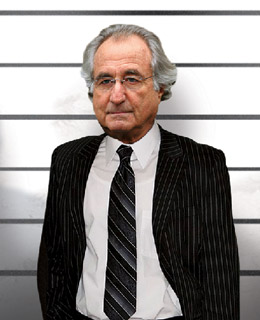

Photo Illustration; Madoff: Andrea Renault / Polaris; Jupiter

His alleged Ponzi scheme could inflict $50 billion in losses on society types, retirees and nonprofits. The bigger cost for America comes from the notion that Madoff pulled off the biggest financial fraud in history right under the noses of regulators. Assuming it's all true, the banks and hedge funds that neglected due diligence were stupid and paid for it, while the managers who fed him clients' money — the so-called feeders — were reprehensibly greedy. But to reveal government and industry regulators as grossly incompetent casts a shadow of doubt far and wide, which crimps the free flow of investment capital. That will make this downturn harder on us all.

Hedge funds played an important role in the shift to sloppy mortgage lending. By buying up mortgage loans, Devaney and other hedge-fund managers made it profitable for lenders to make questionable loans and then sell them off. Hedge funds were more than willing to swallow the risk in exchange for the promise of fat returns. Devaney wasn't just a big buyer of mortgage bonds — he had his own $600 million fund devoted to buying risky loans — he was one of its cheerleaders. Worse, Devaney knew the loans he was funding were bad for consumers. In early 2007, talking about option ARM mortgages, he told Money, "The consumer has to be an idiot to take on one of those loans, but it has been one of our best-performing investments."

For years, the worst moniker you heard thrown at Goodwin, the former boss of Royal Bank of Scotland (RBS), was "Fred the Shred," on account of his knack for paring costs. A slew of acquisitions changed that, and some RBS investors saw him as a megalomaniac. Commentators have since suggested that Goodwin is simply "the world's worst banker." Why so mean? The face of over-reaching bankers everywhere, Goodwin got greedy. More than 20 takeovers helped him transform RBS into a world beater after he assumed control in 2000. But he couldn't stop there. As the gloom gathered in 2007, Goodwin couldn't resist leading a $100 billion takeover of Dutch rival ABN Amro, stretching RBS's capital reserves to the limit. The result: the British government last fall pumped $30 billion into the bank, which expects 2008 losses to be the biggest in U.K. corporate history.

Who decided banks had to be all things to all customers? Weill did. Starting with a low-end lender in Baltimore, he cobbled together the first great financial supermarket, Citigroup. Along the way, Weill's acquisitions (Smith Barney, Travelers, etc.) and persistent lobbying shattered Glass-Steagall, the law that limited the investing risks banks could take. Rivals followed Citi. The swollen banks are now one of the country's major economic problems. Every major financial firm seems too big to fail, leading the government to spend hundreds of billions of dollars to keep them afloat. The biggest problem bank is Weill's Citigroup. The government has already spent $45 billion trying to fix it.

In his two decades as Iceland's Prime Minister and then as central-bank governor, Oddsson made his tiny country an experiment in free-market economics by privatizing three main banks, floating the currency and fostering a golden age of entrepreneurship. When the market turned ... whoops! Iceland's economy is now a textbook case of macroeconomic meltdown. The three banks, which were massively leveraged, are in receivership, GDP could drop 10% this year, and the IMF has stepped in after the currency lost more than half its value. Nice experiment.

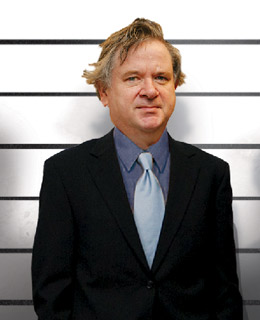

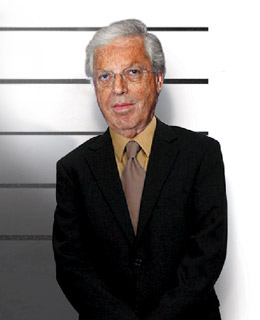

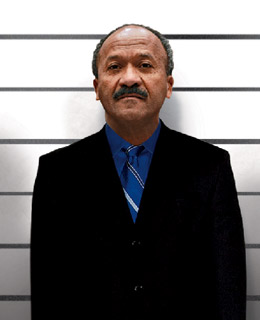

Photo Illustration; Cayne: Oscar Hidalgo / New York Times / Redux; Getty

Plenty of CEOs screwed up on Wall Street. But none seemed more asleep at the switch than Bear Stearns' Cayne. He left the office by helicopter for 3 ½-day golf weekends. He was regularly out of town at bridge tournaments and reportedly smoked pot. (Cayne denies the marijuana allegations.) Back at the office, Cayne's charges bet the firm on risky home loans. Two of its highly leveraged hedge funds collapsed in mid-2007. But that was only the beginning. Bear held nearly $40 billion in mortgage bonds that were essentially worthless. In early 2008 Bear was sold to JPMorgan for less than the value of its office building. "I didn't stop it. I didn't rein in the leverage," Cayne later told Fortune.

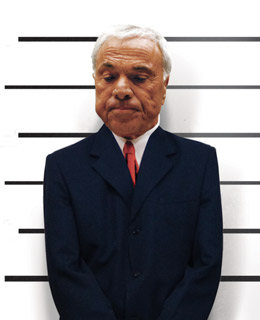

Photo Illustration; Mozillo: Mark Wilson / Getty; Getty

The son of a butcher, Mozilo co-founded Countrywide in 1969 and built it into the largest mortgage lender in the U.S. Countrywide wasn't the first to offer exotic mortgages to borrowers with a questionable ability to repay them. In its all-out embrace of such sales, however, it did legitimize the notion that practically any adult could handle a big fat mortgage. In the wake of the housing bust, which toppled Countrywide and IndyMac Bank (another company Mozilo started), the executive's lavish pay package was criticized by many, including Congress. Mozilo left Countrywide last summer after its rescue-sale to Bank of America. A few months later, BofA said it would spend up to $8.7 billion to settle predatory lending charges against Countrywide filed by 11 state attorneys general.

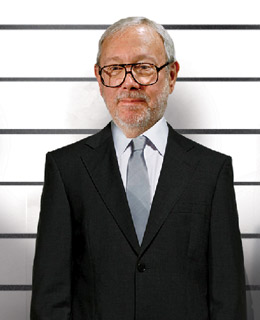

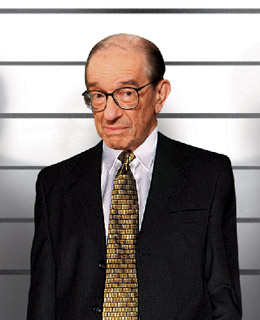

Alan Greenspan

Photo Illustration; Greenspan: Alex Wong / Getty; Getty

The Federal Reserve chairman — an economist and a disciple of libertarian icon Ayn Rand — met his first major challenge in office by preventing the 1987 stock-market crash from spiraling into something much worse. Then, in the 1990s, he presided over a long economic and financial-market boom and attained the status of Washington's resident wizard. But the super-low interest rates Greenspan brought in the early 2000s and his long-standing disdain for regulation are now held up as leading causes of the mortgage crisis. The maestro admitted in an October congressional hearing that he had "made a mistake in presuming" that financial firms could regulate themselves.

EX

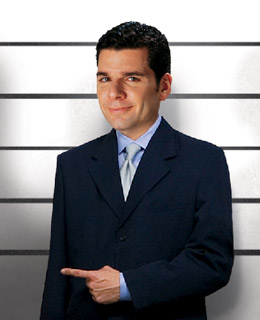

Chris Cox

Photo Illustration; Cox: Roger L. Wollenberg / Landov: Getty

The ex-SEC chief's blindness to repeated allegations of fraud in the Madoff scandal is mind-blowing, but it's really his lax enforcement that lands him on this list. Cox says his agency lacked authority to limit the massive leveraging that set up last year's financial collapse. In truth, the SEC had plenty of power to go after big investment banks like Lehman Brothers and Merrill Lynch for better disclosure, but it chose not to. Cox oversaw the dwindling SEC staff and a sharp drop in action against some traders.

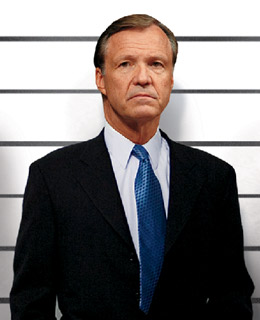

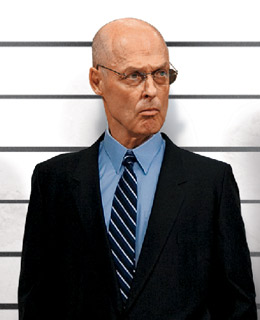

Hank Paulson

Photo Illustration; Paulson: Susan Walsh / AP; Getty

When Paulson left the top job at Goldman Sachs to become Treasury Secretary in 2006, his big concern was whether he'd have an impact. He ended up almost single-handedly running the country's economic policy for the last year of the Bush Administration. Impact? You bet. Positive? Not yet. The three main gripes against Paulson are that he was late to the party in battling the financial crisis, letting Lehman Brothers fail was a big mistake and the big bailout bill he pushed through Congress has been a wasteful mess.

Photo Illustration; Cassano: Keith Waldgrave / Zuma; Getty

Before the financial-sector meltdown, few people had ever heard of credit-default swaps (CDS). They are insurance contracts — or, if you prefer, wagers — that a company will pay its debt. As a founding member of AIG's financial-products unit, Cassano, who ran the group until he stepped down in early 2008, knew them quite well. In good times, AIG's massive CDS-issuance business minted money for the insurer's other companies. But those same contracts turned out to be at the heart of AIG's downfall and subsequent taxpayer rescue. So far, the U.S. government has invested and lent $150 billion to keep AIG afloat.

NEXT

Phil Gramm

Photo Illustration; Gramm: Douglas Healey / AP; Getty

As chairman of the Senate Banking Committee from 1995 through 2000, Gramm was Washington's most prominent and outspoken champion of financial deregulation. He played a leading role in writing and pushing through Congress the 1999 repeal of the Depression-era Glass-Steagall Act, which separated commercial banks from Wall Street. He also inserted a key provision into the 2000 Commodity Futures Modernization Act that exempted over-the-counter derivatives like credit-default swaps from regulation by the Commodity Futures Trading Commission. Credit-default swaps took down AIG, which has cost the U.S. $150 billion thus far.

Homebuilders had plenty to do with the collapse of the housing market, not just by building more homes than the country could stomach, but also by pressuring people who couldn't really afford them to buy in. As CEO of Beazer Homes since 1994, McCarthy has become something of a poster child for the worst builder behaviors. An investigative series that ran in the Charlotte Observer in 2007 highlighted Beazer's aggressive sales tactics, including lying about borrowers' qualifications to help them get loans. The FBI, Department of Housing and Urban Development and IRS are all investigating Beazer. The company has admitted that employees of its mortgage unit violated regulations — like down-payment-assistance rules —at least as far back as 2000. It is cooperating with federal investigators.

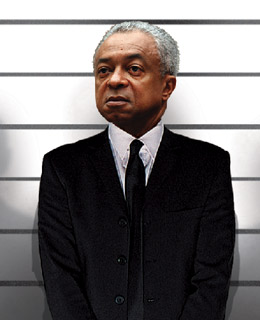

Photo Illustration; Raines: Jason Reed / Landov; Jupiter

The mess that Fannie Mae has become is the progeny of many parents: Congress, which created Fannie in 1938 and loaded it down with responsibilities; President Lyndon Johnson, who in 1968 pushed it halfway out the government nest and into a problematic part-private, part-public role in an attempt to reduce the national debt; and Jim Johnson, who presided over Fannie's spectacular growth in the 1990s. But it was Johnson's successor, Raines, who was at the helm when things really went off course. A former Clinton Administration Budget Director, Raines was the first African-American CEO of a Fortune 500 company when he took the helm in 1999. He left in 2004 with the company embroiled in an accounting scandal just as it was beginning to make big investments in subprime mortgage securities that would later sour. Last year Fannie and rival Freddie Mac became wards of the state.

Photo Illustration; Corbet: Laura Cavanaugh / Landov: Jupiter

By slapping AAA seals of approval on large portions of even the riskiest pools of loans, rating agencies helped lure investors into loading on collateralized debt obligations (CDOs) that are now unsellable. Corbet ran the largest agency, Standard & Poor's, during much of this decade, though the other two major players, Moody's and Fitch, played by similar rules. How could a ratings agency put its top-grade stamp on such flimsy securities? A glaring conflict of interest is one possibility: these outfits are paid for their ratings by the bond issuer. As one S&P analyst wrote in an email, "[A bond] could be structured by cows and we would rate it."

Photo Illustration; Fuld: Kevin Lamarque / Landov: Getty

The Gorilla of Wall Street, as Fuld was known, steered Lehman deep into the business of subprime mortgages, bankrolling lenders across the country that were making convoluted loans to questionable borrowers. Lehman even made its own subprime loans. The firm took all those loans, whipped them into bonds and passed on to investors billions of dollars of what is now toxic debt. For all this wealth destruction, Fuld raked in nearly $500 million in compensation during his tenure as CEO, which ended when Lehman did.

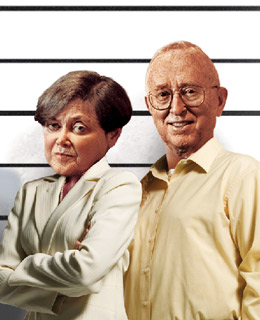

Photo Illustration; Sandlers: Elena Dorfman / Redux; Corbis

In the early 1980s, the Sandlers' World Savings Bank became the first to sell a tricky home loan called the option ARM. And they pushed the mortgage, which offered several ways to back-load your loan and thereby reduce your early payments, with increasing zeal and misleading advertisements over the next two decades. The couple pocketed $2.3 billion when they sold their bank to Wachovia in 2006. But losses on World Savings' loan portfolio led to the implosion of Wachovia, which was sold under duress late last year to Wells Fargo.

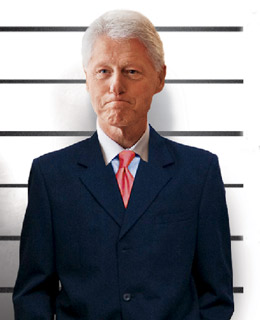

President Clinton's tenure was characterized by economic prosperity and financial deregulation, which in many ways set the stage for the excesses of recent years. Among his biggest strokes of free-wheeling capitalism was the Gramm-Leach-Bliley Act, which repealed the Glass-Steagall Act, a cornerstone of Depression-era regulation. He also signed the Commodity Futures Modernization Act, which exempted credit-default swaps from regulation. In 1995 Clinton loosened housing rules by rewriting the Community Reinvestment Act, which put added pressure on banks to lend in low-income neighborhoods. It is the subject of heated political and scholarly debate whether any of these moves are to blame for our troubles, but they certainly played a role in creating a permissive lending environment.

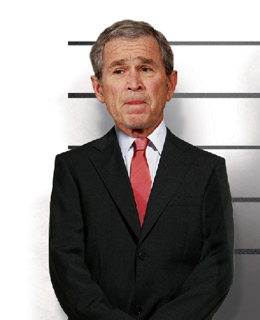

Photo Illustration; Bush: Jason Reed / Reuters; Getty

From the start, Bush embraced a governing philosophy of deregulation. That trickled down to federal oversight agencies, which in turn eased off on banks and mortgage brokers. Bush did push early on for tighter controls over Fannie Mae and Freddie Mac, but he failed to move Congress. After the Enron scandal, Bush backed and signed the aggressively regulatory Sarbanes-Oxley Act. But SEC head William Donaldson tried to boost regulation of mutual and hedge funds, he was blocked by Bush's advisers at the White House as well as other powerful Republicans and quit. Plus, let's face it, the meltdown happened on Bush's watch.

Merrill Lynch's celebrated CEO for nearly six years, ending in 2007, he guided the firm from its familiar turf — fee businesses like asset management — into the lucrative game of creating collateralized debt obligations (CDOs), which were largely made of subprime mortgage bonds. To provide a steady supply of the bonds — the raw pork for his booming sausage business —O'Neal allowed Merrill to load up on the bonds and keep them on its books. By June 2006, Merrill had amassed $41 billion in subprime CDOs and mortgage bonds, according to Fortune. As the subprime market unwound, Merrill went into crisis, and Bank of America swooped in to buy it.

Photo Illustration; Jiabao: Oli Scarff / AP; Getty

Think of Wen as a proxy for the Chinese government — particularly those parts of it that have supplied the U.S. with an unprecedented amount of credit over the past eight years. If cheap credit was the crack cocaine of this financial crisis — and it was — then China was one of its primary dealers. China is now the largest creditor to the U.S. government, holding an estimated $1.7 trillion in dollar-denominated debt. That massive build-up in dollar holdings is specifically linked to China's efforts to control the value of its currency. China didn't want the renminbi to rise too rapidly against the dollar, in part because a cheap currency kept its export sector humming — which it did until U.S. demand cratered last fall.

Photo Illustration; Lereah: Kevin Dietsch / Landov; Corbis

When the chief economist at the National Association of Realtors, an industry trade group, tells you the housing market is going to keep on chugging forever, you listen with a grain of salt. But Lereah, who held the position through early 2007, did more than issue rosy forecasts. He regularly trumpeted the infallibility of housing as an investment in interviews, on TV and in his 2005 book, Are You Missing the Real Estate Boom?. Lereah says he grew concerned about the direction of the market in 2006, but consider his January 2007 statement: "It appears we have established a bottom."

A feud lasting nearly four decades between a Virginia lawyer and the Virginia State Bar (VSB) is coming to a head Daniel and the VSB Rhetta Daniel has been practicing law in Virginia for almost forty years; from 1982 - 1920 she worked as a Senior Assistant Bar Counsel for the VSB, prosecuting bad lawyers for them. These proceedings could lead to the removal of a lawyer's license to practice law, and as such their ability to continue to practice law. Daniel said she was pushed out as the Senior Assistant Bar Counsel in 1990 after it became clear that her aggressive style was not welcome and that the VSB was more interested in protecting connected attorneys than weeding out unscrupulous ones. The specific case was My Linh Soland, a client who had two powerful lawyers. "What they did was protect her defense counsel," Daniel said. She explained that a letter that may have doctored the attorney's letterhead was in the possession of her...

The State of Pennsylvania "Cash for the Elderly" is MURDERING the elderly for the profit of Judges "friends" Genevieve Bush 89 of Chester County, Pennsylvania Before the Guardianship Today Nearly a decade in, Genevieve Bush, 89, continues to be held in guardianship against her will, against advanced directives, her life savings is nearly depleted. The Estate Battle Bush’s saga started approximately fifteen years ago, when Genevieve Bush’s sons, Joseph and Michael, challenged the estate of her and her husband. After her husband had a stroke and was hospitalized in November 2003, they saw an opening, according to a letter she wrote in 2007, to her brother Leon. “In April 2004, before Fabian (her husband) passed, Joseph asked me to sign a blank check…Joe asked me to sign more blank checks so he could move the money…In May of 2005, Joe called me and told me he was putting stocks in my name…Then, (a) month later in June, Joe ...

Should a Judge be allowed to steal a child from a Mother without knowing the full story and Lawyers gaslighting and or not telling the whole TRUTH of the issues A Virginia Mom faces the loss of her parental rights for a son she primarily raised for the first six years of his life. The Set Up Natalia Dalton in the City of Alexandria, Virginia spent the first six years of her sons life as his primary caregiver. She and her ex-boyfriend Julio LaCayo had a son in 2008. They were never married, and custody was always arranged in some part through court orders the entirety of her son’s life. For the first six years of his life, Natalia had physical custody, her son thrived in school under her care. “There was one court hearing during that time over the sons passport.” Dalton noted. In 2013, that all changed. Indeed, t...

THE GRAND JURY An Independent ARM of Government not Administrative What is JudicialPedia.com ??? JudicialPedia.com was launched July 4, 2020, by Founder Janice Wolk Grenadier, a place that gives a voice to all Americans. “Make America’s Judiciary Accountable” As we are on the cusp of 2021, I hope you will consider a donation to JudicialPedia.com to “fast and furiously” be able to change the judiciary and bring justice to many Americans who every day are at a loss as to what happened to them in the courtroom. To donate go to the website JudicialPedia.com and donate through PayPal, or Zelle 202-368-7178. Because it has become self-evident that the Judiciary, Governmental and Elected Officials have proven they cannot police themselves: Our goal is to ensure that the American people are given Justice Evenly and Fairly without prejudice... The end result will bring us back to justice and take care of the waste of tax dollars and the many who are falsel...

Do you have a Mortgage? Did you know it may not really exist THIS IS A "TRILLION" Dollar "SCAM" on HOMEOWNERS & PENSIONS of "Main Street" America Did you know your Mortgage Payments go to "SHELL BANKS" & "FAKE MBS" that then go to large "BONUS" and "INSIDER TRADING" That all homeowners need to go to their Court house and review every document that has been filed against your home. It is the Attorney General of your State that has received over $1 BILLION to prevent these Frauds from happening The Virginia Attorney General Jason Miyares may have inherited this problem - But, he was elected on his statements that being from "Cuba" and his "Mothers Story" coming here created a " Smoke and Mirrors" that he actually cared- AGAIN we have Lied too in Virginia ...

The “Old Boys Network” of Virginia Doing it Again with the collusion of Judges and Lawyers Ensuring they DRAIN the Estate & Destroy a Family The SCHEME one the “Old Boys Network” of Virginia uses Time and Time again At first blush the case: JACQUELINE BOGLE MEUSE, individually and derivatively on behalf of, ALEXANDRIA INVESTMENTS, LLC, BOGLE INDUSTRIES, INC., KING STREET METRO VENTURE, LLC, 4607 EISENHOWER ASSOCIATES, LLC, 4601 EISENHOWER ASSOCIATES, LLC, and THE IRREVOCABLE BOGLE TRUST, Petitioners – Appellants, v. BRUCE HENRY, individually and as the Co-Trustee of t...

Virginia Legislature - Courts of Justice Virginia Judicial Interviews Go “Off the Rails” “This is a f**king shitshow” when the SECRECY of CHOOSING JUDGES IS CHALLENGED By: The Public THIS SHOWS HOW AND WHERE THE CORRUPTION IN THE COURTS OF VIRGINIA Virginia Courts are RACIST, PREDATORY & DISHONEST Twice a year and maybe more the Courts of Justice of Virginia choices NEW JUDGES and RENEWS old Judges, and the JIRC committee members. This is done as SECRETLY as they can. The information is difficult to find on the site and emails with the times of the meeting are not usually on auto email as other meetings are. You should remember when a complaint of a Judge or lawyer is made all should take it very seriously, in Virginia it is ignored. That Justice in Virginia is only available for the very Rich and Powerful. JudicalPedia.com was launched in July of 2020 to show this. The Dark Side A...

CITY OF ALEXANDRIA POLICE TOOLS OF “THE OLD BOYS” NETWORK OF VIRGINIA THE “BIG LIE” and THE “BIG COVER-UP” “THE TRUTH” of Lawyers & Judges in the City of Alexandria can be found here in this Blog & VALAW2010.Blogspot.com along with JudicialPedia.com https://www.alexandriava.gov/RedactionLog The current Chief of Police for the City of Alexandria is Tarrick McGuire appears to be raciest interesting from Arlington, Texas where are City Manager James Parajon is from and our Governor of Virginia Youngkin appears to have business’s Along with Interim Police Chief now Assistant Chief Raul Pedroso - don’t know the law and or both are paid to “Cover-up” for the City of Alexandria “Elite” Judges & Lawyers who allow “False and Fraudulent" documents to create “Deed Theft” “Hate Crimes” The “FAKE & Fraudulent” Documents that are filed in the City of Alexandria Clerk's office that are supported by:...

You may have seen 15 W. Spring St., Alexandria VA on the Market FOR SALE The SALE is in REVENGE by TROUTMAN PEPPER HAMILTON SANDERS aka MAYS & VALENTINE For EXPOSING Their MANIPULATION and TAMPERING with or STEALING FROM TRUST ACCOUNTS that they MANIPULATED $30.000.00 in 1990 from Janice Wolk Grenadier to COVER-UP TROUTMAN PEPPER HAMILTON SANDERS aka MAYS & VALENTINE - claims to be the lawyer for Wells Fargo Bank -"OOPS" Wells Fargo Bank in taped conversations and when responding to subpoenas had no clue TROUTMAN PEPPER HAMILTON SANDERS aka MAYS & VALENTINE was or is their lawyer Read More: https://judicialpedia.com/listing/criminal-trust-theft-by-lawyer-jim-arthur-of-troutman-pepper-hamilton-sanders-aka-mays-valentine-cover-up-of-trust-theft-by-divorce-lawyer-ilona-ely-freedman-grenadier-heckman-of-sonia-grenadier/ The home was illegally foreclosed on in March of 2018 It was an illegal Foreclosure - Here are the documents to prove it: It has been stated...

Comments

Post a Comment